The Texas legislature has taken a decisive step toward tightening the rules that govern merchant cash advances (MCAs). The bill, which now sits in the Senate after clearing the House, would require all MCA brokers to register with the Office of Consumer Credit Commissioner (OCCC) before they can legally broker deals for merchants operating within state borders. This new layer of oversight is poised to reshape how small businesses access quick capital and could ripple across the broader commercial finance landscape.

While the bill’s text remains under review, industry observers are already weighing its implications. For entrepreneurs seeking fast funding, the move may mean higher compliance costs or a narrower pool of brokers willing to navigate the new paperwork. Conversely, advocates for consumer protection argue that registration will curb predatory practices and increase transparency in an often opaque market.

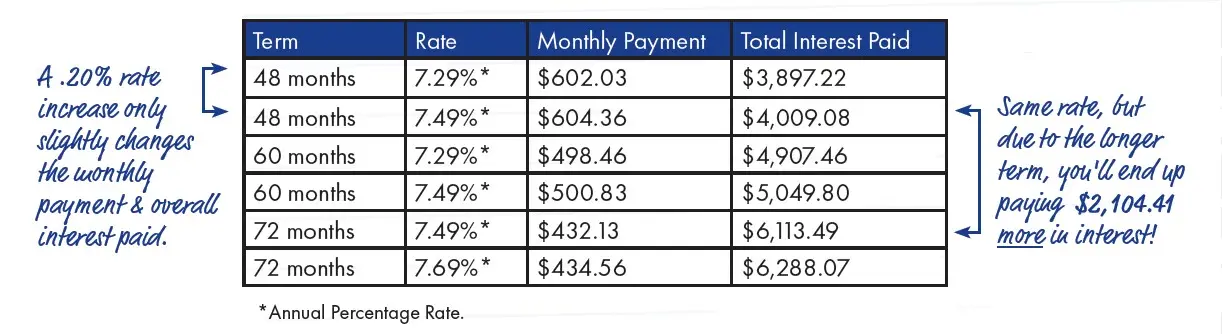

For more detailed coverage on how this legislation could affect your business financing options, check out texasloanstoday.com, a dedicated resource for Texas borrowers seeking up‑to‑date loan insights.

What the MCA Bill Actually Says

The core of the proposal is a broker registration requirement. Under the new rules, any broker who facilitates an MCA for a Texas merchant must secure approval from OCCC. The commission will be empowered to set standards, approve or deny applications, and monitor ongoing compliance.

- Scope: Applies to brokers regardless of where they are physically located; the broker’s office could be in Dallas, Austin, or even out of state.

- Oversight: OCCC will enforce “fair practice” guidelines and can impose sanctions for violations.

- Additional Authority: The Texas Finance Commission gains the power to adopt its own rules targeting unfair acts by providers, potentially covering interest rate caps or disclosure requirements.

The bill’s proponents argue that registration will prevent unscrupulous brokers from exploiting merchants who lack financial literacy. Critics counter that the additional bureaucracy could stifle innovation and push small businesses toward alternative lenders that are not subject to the same oversight.

Industry Reactions

Representatives of the merchant cash advance industry have issued statements warning against what they describe as “over‑regulation.” They point out that many MCAs already operate under state consumer credit laws and argue that the new bill would duplicate existing protections while imposing costly compliance burdens.

Meanwhile, small business advocacy groups are split. Some see registration as a safeguard that could increase trust in the MCA market, citing cases where merchants paid exorbitant fees without clear disclosure. Others fear that stricter rules might reduce the availability of fast capital for startups and seasonal businesses that rely on MCAs to bridge cash‑flow gaps.

How This Bill Fits Into Texas’ Broader Regulatory Landscape

Texas has a history of balancing business-friendly policies with consumer protection. The proposed MCA bill aligns with other recent efforts, such as the state’s push to regulate payday lenders and short‑term loan providers under the Texas Payday Lending Act.

| Regulation | Targeted Industry | Key Requirement |

|---|---|---|

| MCA Broker Registration Bill | Merchant Cash Advances | Brokers must register with OCCC |

| Payday Lending Act Amendments (2024) | Short‑Term Loans | Interest rate caps, disclosure mandates |

| Texas Credit Union Regulatory Oversight (2025) | Credit Unions | Enhanced consumer protection standards |

The convergence of these initiatives suggests a state‑wide push to create clearer, more enforceable standards across all forms of consumer credit. For businesses, this could mean fewer surprises but also a need for greater due diligence when selecting financing partners.

Impact on Small Business Financing Options

With the MCA broker registration requirement in place, small business owners may find themselves turning to alternative funding sources such as:

- Traditional bank loans: Though often slower, banks provide transparent terms and regulatory oversight.

- Online lenders: Many digital platforms offer streamlined application processes but still face increasing scrutiny from regulators.

- Equipment financing: For capital-intensive businesses, leasing or purchasing equipment directly can be a viable alternative.

Each option comes with its own set of pros and cons. Traditional banks may impose stricter credit requirements, while online lenders might offer faster approval but at higher rates. Equipment financing often locks in long‑term payments that could strain cash flow if market conditions shift.

The Bigger Picture: Consumer Protection vs. Market Freedom

At its heart, the debate over MCA regulation is a classic clash between two philosophies:

- Consumer Protection Advocates: Argue that unregulated markets lead to predatory practices, hidden fees, and unfair contract terms.

- Market Freedom Proponents: Stress that too much regulation stifles innovation, raises costs, and reduces access for the very businesses that need quick capital.

Both sides present valid concerns. The outcome will likely hinge on how OCCC balances enforcement with flexibility, perhaps by offering a tiered registration system based on broker volume or risk profile.

Looking Ahead: Potential Amendments and Implementation Challenges

If the bill passes, implementation could face logistical hurdles:

- Registration Process: Brokers will need to submit documentation proving financial stability, compliance training records, and background checks.

- OCCC Resources: The commission may require additional staff or technology upgrades to manage the influx of registrations and ongoing audits.

- Legal Challenges: Some industry groups might file lawsuits claiming that the bill violates free‑speech or commerce provisions, potentially delaying enforcement.

These challenges underscore the need for a phased rollout. A pilot program could test registration procedures on a smaller scale before full implementation.

How to Stay Informed and Prepare Your Business

- Track Legislative Updates: Subscribe to Texas legislative newsletters or follow OCCC’s official announcements for real‑time changes.

- Review Current Financing Agreements: Ensure that any existing MCA contracts comply with forthcoming regulations, especially regarding disclosure and fee limits.

- Build Relationships with Multiple Lenders: Diversifying funding sources mitigates risk if one channel becomes restricted or more costly.

By staying proactive, businesses can navigate the evolving regulatory environment without sacrificing access to essential capital. Whether you’re a seasoned entrepreneur or just launching your first venture, understanding how these changes impact loan terms and broker relationships is crucial for long‑term financial health.

Additional Resources for Texas Borrowers

- Money’s Mortgage Rates Dashboard: Offers up-to-date mortgage rate trends that can inform broader borrowing decisions.

- Freddie Mac’s Weekly Rate Reports: Provides benchmark rates for conventional loans, useful for comparing MCA costs against standard financing options.

Staying informed through reputable sources and engaging with local regulatory bodies will help you adapt to the new landscape and secure the best possible terms for your business’s financial needs.